Fixing Your Finances Part 4. Which Debts You Should Pay Off First

We’re finally there! You’ve made a budget, investigated cutbacks, and looked at earning a little extra. Today we’re going to talk about the best way to make use of the extra cash. So, let’s look at which debts you should pay off first?

You’ve come such a long way! You’ve done all the hard work making a budget and keeping a spending diary. You’ve been honest with yourself about what you do and don’t need. Finally, you’ve investigated other ways you can bring in a little extra cash. That’s a lot of work so you should be proud of all the effort you’ve put in up to this point.

By now, you should know how much you have per month to pay down your debts. The last step is choosing the most effective way to do it. If you only have one credit card it’s pretty easy, pay it! If you have several debts across credit cards, store cards, catalogues and loans, though, it can be more difficult. Fear not though, I’m here to help. Here’s how to decide which debts you should pay off first.

Yes, Another List!

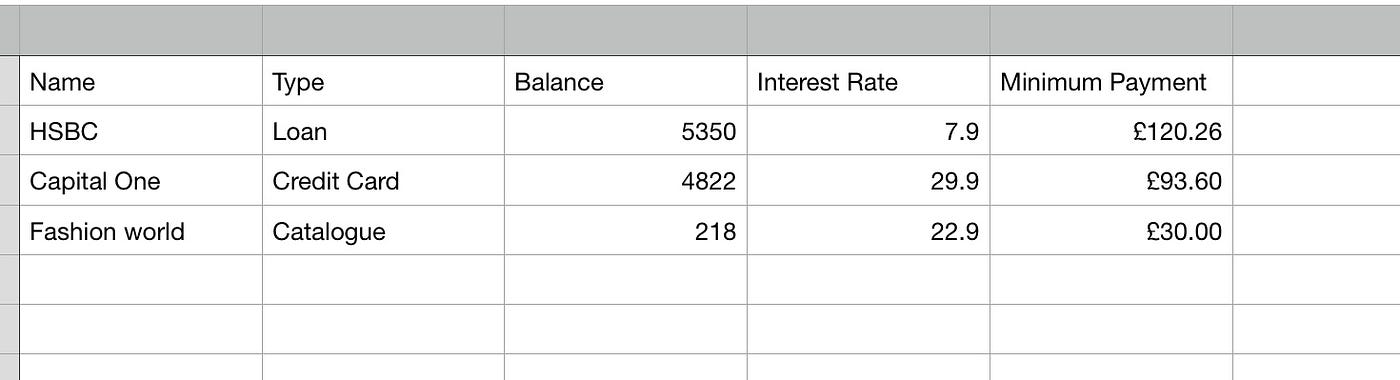

The first thing to do is make a list of all your debts. Note down what they are (Lloyds credit card, John Lewis store card, Halifax loan etc). Record their current balance, the minimum payment, and what the interest rate is. Yes I know, another list! I love lists can you tell? They are one of the best, if not the best, ways to get organised.

Once you’ve got your list then there are a couple of ways to approach it. The conventional wisdom is to choose the one that is costing you the most in interest and pay it off first. This does make perfect sense. The higher the interest the more it costs you. If you pay it down then it’s costing you less. A no-brainer, right? The only alternative suggestion I would make is to look for quick wins first.

You may be feeling depressed, or even a bit scared, when you look at how much you owe. You’re thinking about how long it’s going to take to pay off. What you’ll have to go without to keep the money coming in to service these debts.

You might be feeling like an idiot to let it get to this point. The antidote to all these negative thoughts is a victory. Something that shows you that you can do this.

Quick Wins

That’s why I suggest checking your list and start by picking one of the smallest debts first. For example, one of your debts might be £200 to a catalogue. Let’s say you’ve worked out you can spend £100 on top of the minimum monthly payments for all your debts. If you put it towards the catalogue that debt will be gone in 2 months. You can strike it off your list. Or delete it from your spreadsheet. One debt is already gone from your life. It’s one less thing to worry about. Believe me, it feels great!

Once that one debt is gone you’ll feel better. You’ll have proved to yourself you can do it. That one debt is the first step in building momentum to clear it all. Now you can move on to the rest. At this point, when choosing which debts you should pay off first I would recommend choosing the debt with the highest interest and putting as much as you possibly can towards it.

Even if in the past you’ve paid more than the minimum to your other debts stop doing that for now. Pay the minimum to the others and put every penny towards this one. Once the debt with the highest interest is repaid keep working your way down the list until they’re all gone. One warning though…

No more debt!

The point of this work is to get you debt-free. That means you need to treat your credit cards like they do not exist from now on. They are not an option for any future spending. Cut them up!

Before you start paying off your debts you need to be sure your budget is correct. There’s no point cutting back to pay more to your debts if you’re not leaving yourself enough to live on every month. Spending more than you earn is how you ran up your balances in the first place. Make sure your budget is realistic and has a little wiggle room for unforeseen expenses.

A Note on Balance Transfers and Consolidation Loans

A lot of people who have large amounts of outstanding debt are lured by the idea of taking out a loan to clear everything. Then they’re left with 1 single payment often with a lower interest rate. The question of which debts you should pay off first becomes irrelevant, right?

Possibly! This can be a workable idea. Only if you know you’re going to be disciplined, though! Taking out a consolidation loan is a very common theme on forums where posters are in a very bad financial position.

It’s a great idea if you know you will close every single account your pay off. NO excuses! In many cases though, the posters didn’t. They kept them “for emergencies” and promised themselves they wouldn’t use them. The problem was they had only just started their debt-free journey. They hadn’t built the habits of living within their means. They hadn’t worked out the kinks and omissions in their budget.

What happened? I’m sure, dear reader, that you’re smart enough to figure it out. They started spending on the credit cards again. In a relatively short time, they had run up large balances and now they had a large loan payment to make too. Their finances went downhill pretty quickly from there! This is why I would advise you to only consider it once you’re a bit further along the road. Once you know you’ll close the accounts you’ve paid off and not increase your debt by a penny.

The same is true for balance transfer credit cards. Used properly, these are an extremely useful tool. You move your debt to another card that will charge you no interest for a year or more. This means every penny you pay off goes to clearing the debt. If you have a good enough credit rating to get a good deal then do it. However, do it only if you’re going to close your old account immediately! Leave no avenues for temptation. If you aren’t sure what deals you may qualify for moneysavingexpert.com has a page that will help you. It will find you the best deal and tell you how likely you are to be accepted.

TL:DR

The 4 steps you need to follow are :

- Create a budget of all your outgoings including monthly payments to debts. Keep a spending diary if you don’t know where cash is going.

- Study your budget and figure out if there’s anything you can cancel. You should also look to switch deals on your utilities, tv, internet etc to find a cheaper deal

- Look into any ways to earn extra money. This could be cashback, selling stuff you no longer use, or getting a second job.

- Once you know how much you have monthly make a list of all your debts and pay off the one with the highest interest first. Once that’s paid move on to the next one.

That’s it! The end of this 4-part series. I hope you find it helpful. If you have any questions or comment please get in touch. I’m always happy to help 🙂